Community banks serve as both trusted pillars within their communities and drivers of commerce for their local economies. Last year, we launched BNY’s Voice of Community Banks initiative through an inaugural survey and white paper to assess the state of community banks nationwide, uncovering distinct challenges they face and promising opportunities to help them grow. Since then, we have engaged with community banks across the country, deepening our understanding of their needs and reaffirming our commitment to support U.S. communities.

At BNY, our work is primarily guided by our strategic pillar, Be More for Our Clients, which encourages our people to grow with our clients and consistently innovate our solutions to capture emerging trends so we can best serve them. In our engagements with community banks, we find this guiding principle is present throughout the work they do, too, especially with the businesses they serve.

Given our role as a solutions provider for businesses and organizations, we understand the value of knowing business clients’ needs, from product offerings to engagement feedback. This also applies to our work with community banks, which is why we included small business executives in this year’s survey to provide a view of their needs, experiences and opportunities for collaboration with community banks.

Our survey this year revealed community bankers see small businesses as their primary client, and providing innovative banking solutions to these clients is an integral part of their business models. This paper delves into takeaways from the survey and highlights opportunities that community banks can pursue to best serve their small business clientele.

BNY’s role at the heart of the financial system provides us with a unique opportunity to leverage our expertise and capabilities to help empower the financial communities that shape a strong economy. Our recent commitment to drive deeper financial education for 1,000 community banks across the country underscores our dedication to helping U.S. communities flourish. Through sessions led by BNY subject matter experts, we aim to share knowledge and our experiences on key topics that are essential to long-term success in the banking sector.

As we head into America’s 250th anniversary next year, we are more eager than ever to increase contributions to the prosperity of our national economy.

The Community Banking & Solutions Team

Sarah Atkinson

Chief of Staff to the CEO

Shofiur Razzaque

Head of Community Banking & Solutions

Rashad Townsend

Senior Associate, Community

Banking & Solutions

TOP 5 SURVEY TAKEAWAYS

1

Community Banks Can Expect an Uptick in Demand from Small Business Clientele

About 30% of the small businesses that participated in our survey currently do business with community banks, and 55% said they plan to begin or expand a relationship with a community bank. This finding presents an opportunity for community banks to capitalize on this increased interest with expanded services and new strategies.

2

Community Banks That Prioritize Operational Efficiency See Commercial Impact

More than 80% of community bank small business clients in our survey cited at least one instance of operational inefficiency affecting their experience. Our study also found that community banks that were growing their small business clientele were 81% more likely to digitize manual processes and 49% were more likely to invest in AI to improve operational efficiency.

3

Credit Card Offerings Are a Big Opportunity to Attract Small Business Clients

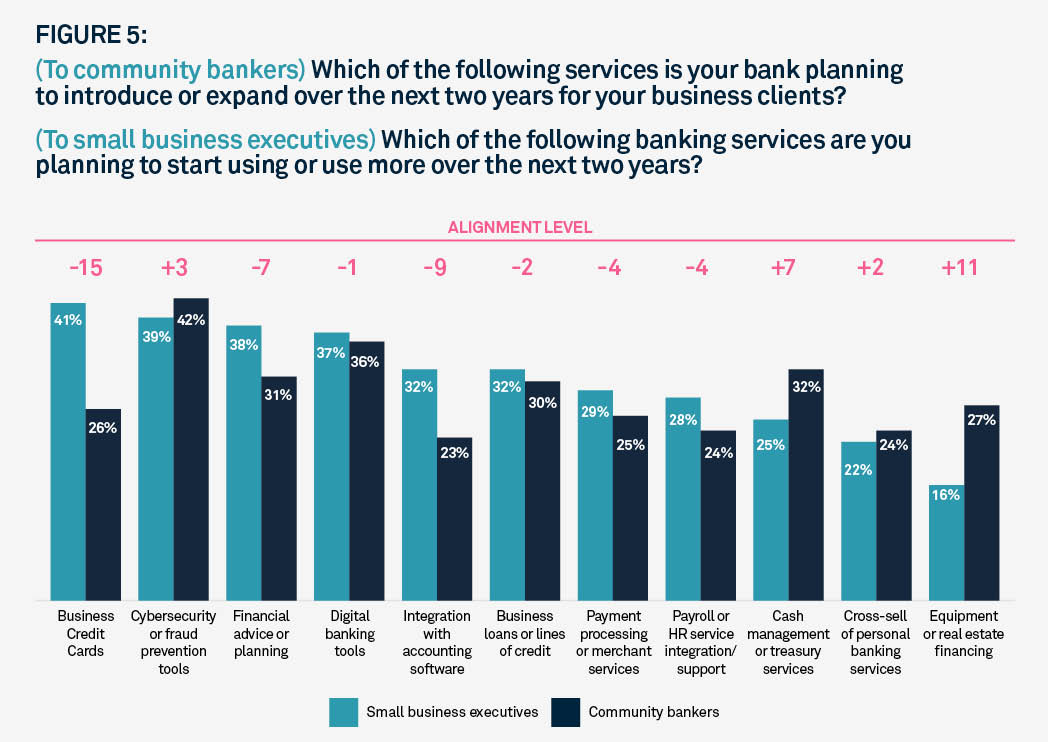

Over 40% of small businesses said they were planning to expand credit card usage, yet only 26% of community banks reported plans to introduce or expand credit card services. Small businesses’ increased reliance on credit card funding highlights an opportunity for community banks to meet service gaps.

4

Strong Risk Management Is a Key Differentiator

Over half of small businesses that ended relationships with community banks cited security concerns as the primary reason. Community banks that saw an increase in small business clientele were over 50% more likely to prioritize such tasks as stress testing and employee training to enhance their cybersecurity protections.

5

Technology and Product Investments Are Top of Mind for 2026

Our survey shows that significant investments from community banks in AI, cybersecurity and fraud prevention, and digital banking capabilities will be top of mind next year. For example, of the 23% of community banks that plan to invest in modern payments, nearly 50% rank the capability as their top investment priority.

CHAPTER 1: THE STATE OF COMMUNITY BANKS IN 2025

Community banks continue to excel on a national scale. According to the Conference of State Bank Supervisors’ Community Bank Sentiment Index,1 the overall outlook from community bankers, encompassing categories like business conditions and bank performance, remains positive and reached its highest level at 126 since the study’s inception in 2019. The FDIC Q2 2025 Report2 underscores this optimism: Compared to last year, community banks experienced 8.5% growth in net income, and around 5% growth in loan and lease balances, as well as domestic deposits.

Community banks have also received significant support from federal and state lawmakers this year. Congressman French Hill, a former community banker, was appointed chair of the House Financial Services Committee and has made advocacy for community banks a central part of his agenda. Additionally, community development financial institutions (CDFIs), including community development banks, generally receive bipartisan support, emphasizing their vital importance to local communities.3

“The need for relationship-driven, locally focused financial services has never been greater. As a CDFI, Southern Bancorp sees this demand even more acutely — and we’re doubling down on our mission to support underserved communities while maintaining our focus on strong financial performance.”

- Darrin Williams, Chief Executive Officer, Southern Bancorp

Despite the optimism, community banks continue to face challenges when providing banking services to their localities. This year’s study reveals that cybersecurity threats, access to capital and liquidity, and adequate data management remain top challenges for community banks, which also came through in BNY’s 2024 Voice of Community Banks Survey.

Regulatory compliance and the ability to embrace digital transformation rose as top challenges for community banks, potentially due to talent and training gaps. Roughly 1 in 4 banks reported difficulties in attracting compliance and tech talent, along with 35% of banks indicating that training on digital platforms was the most critical training need. Additionally, 38% of banks reported that compliance or regulatory risk — the most selected option — was the primary barrier to mitigating operational challenges.

Survey responses show that, over the past five years, community banks have prioritized investments in areas where they feel the most challenged, with roughly 1 in 4 banks having made substantial investments in cybersecurity and fraud prevention, modernization of payments and core banking systems. Additionally, 20% have invested in data analytics and business intelligence tools.

In a competitive environment, investments like these enable community banks to attract and retain clients in their respective markets. Small business clients, ranging from brick-and-mortar retailers to professional service providers, were selected as the primary customer segment for community banks. Each type of small business has continuously evolving needs as they maintain and grow. Through our survey, we aimed to learn more about these needs and emerging demands — and pinpoint where community banks can best fill gaps.

CHAPTER 2: BEING MORE FOR SMALL BUSINESS CLIENTS

A Look at Current Relationships with Community Banks

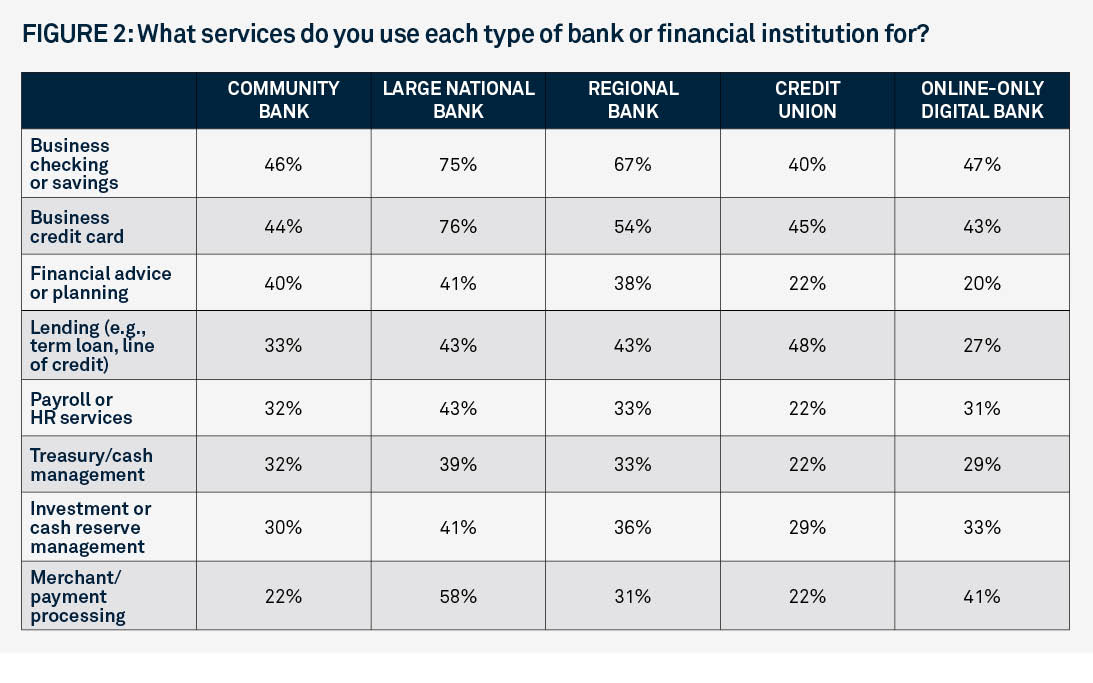

Our survey data highlights the significant relationship between small businesses and community banks. Roughly 30% of small businesses reported that they used community banks for at least one banking service, and half of them said their community bank is their primary banking provider. Our survey shows that small businesses leverage community banks at nearly the same rate for treasury management and financial advising services, but merchant services and business credit cards stood out as key areas where community banks can increase their market share. Notably, community banks face increased competition for these offerings from both non-bank issuers and fintech providers, as well as larger banks.

Reasons varied as to why small business executives chose to leverage a community bank for a particular service over other banks, but the central theme for opting to work with a community bank was clear — satisfaction with client service.

When asked why small business executives leveraged community banks for select services, they noted that they appreciated the personalized service they received for transaction accounts and payroll services, and strong relationships with banking staff helped drive satisfaction with treasury management and financial planning services.

“At the community bank, I am able to resolve any issue face to face, and people are always welcoming and willing to work with you. They are not hard to reach.”

- Small business owner in hospitality

Across the board, small businesses that opted to leverage other providers primarily cited pre-existing relationships, followed by more competitive pricing.

Despite these barriers, there is significant untapped potential for community banks. More than 70% of small businesses said they prefer or would prefer to bank with a community bank, even though only 31% currently do. This points to a clear opportunity for community banks to capture a greater share of the small business market by addressing inefficiencies and strengthening their value proposition.

Barriers to Small Business Satisfaction

Being more for your business clients involves soliciting and acting on feedback that can most effectively illuminate areas of opportunity to improve service. Our survey shows that small businesses are largely satisfied with the services provided to them by the combination of banks they use. However, those that rely primarily on community banks report lower levels of satisfaction when it comes to transparency around terms and fees, as well as emerging technology offerings.

Despite this feedback, 95% of community bankers believe their banks will be able to keep pace with product offerings in the next five years. This sentiment is largely driven by strong leadership commitment (38%) and understanding emerging technologies (36%), yet the least selected option was a dedicated budget (18%), highlighting the persistent challenges smaller banks face when looking to enhance their capabilities.

As community banks tend to be cost constrained, a lack of financial resources can lead to operational exposure and reputational risk. Over half (54%) of small business executives that terminated relationships with community banks cited security concerns as the primary reason. Studies show smaller banks are at a disadvantage when it comes to public perception regarding cybercrime, leading to a strain on current and potential business for the larger community banking sector.

According to a Global Association of Risk Professionals study,4 “cyberattacks [at small banks] generate deposit spillovers to branches of unaffected large banks. Essentially, cyberattacks led to a ‘flight-to-reputation’ effect as larger, more reputable banks are likely to be seen by depositors as more secure against cyberattacks.” Additionally, the same study noted that unaffected small banks did not benefit from the same deposit spillover.

Our survey also suggests that operational challenges at community banks can have a significant impact on perception among small business executives. Over 80% of small business clients of community banks cited at least one instance of their bank’s inefficiency, such as slower turnaround times and a lack of communication, impacting their experience.

The Commercial Impact of Improved Operational Efforts

Regardless of these hurdles, 55% of small businesses plan to begin or expand a relationship with a community bank in the future, indicating recognized value and opportunity to capture demand.

“I think it is fairly rampant that a lot of people still want to bank with community banks. The issue is what the community bank is offering versus the bank down the street."

- Community banker in Louisiana

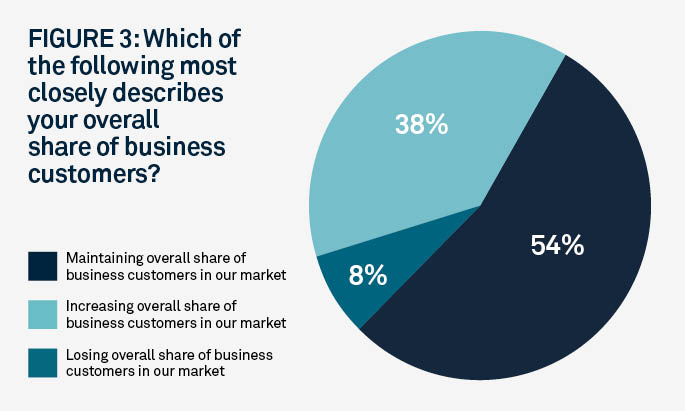

Community banks are always competing for customers, amongst themselves and with other types of banks. To glean insights on potential competitive advantages, we asked community banking executives whether their banks were increasing, maintaining or losing their share of small business customers in their local market. Of our sample, 38% reported they were increasing their overall share of business customers, while 62% were maintaining or losing share.

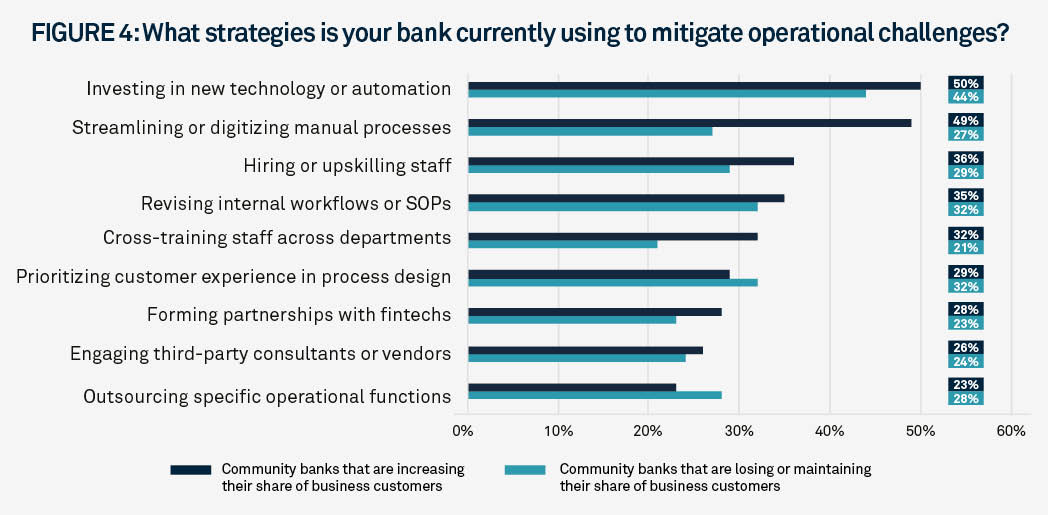

For those increasing their share, we wanted to learn more about the strategic ways they’ve enabled growth in their markets. Given security and operational efficiencies were key concerns for small business clients in our study, we found that community banks with growing small business clientele reported having made substantial efforts to improve in both areas.

Regarding cybersecurity, banks with growing small business clientele were more likely than banks maintaining or losing clients to have taken measures to enhance their protection measures, having performed significantly more auditing and stress testing (63% vs. 38%), as well as employee training (65% vs. 42%), to ensure safety. Additionally, 50% of bankers in this group plan to further expand cybersecurity services within the next two years, while only 37% of banks losing or maintaining small businesses have plans to do so. Robust security and fraud capabilities can enable community bankers to maximize efforts in their most valuable asset — the personal touch.

One small business owner in the risk management industry echoed these sentiments: “The community bank is more personal. We had a debit card issue and they drove [a new] one to us that same day. That's the way we do business — very white glove.”

Banks that are growing their small business clientele were also more proactive in mitigating operational inefficiencies compared to their counterparts. Although both groups reported investing in technology and automation at nearly the same rate, banks with increasing small business clients were 81% more likely (49% vs. 27%) to report digitizing manual processes, along with being nearly 50% more likely (32% vs. 21%) to report cross-training staff across departments. Furthermore, banks that were gaining small business customers were 49% more likely to invest in AI for operational efficiency than their counterparts.

According to Statista, AI spend is increasing at a 29% compound annual growth rate,5 so it makes sense that many community banks are eager to leverage AI, but most have not yet integrated it into their core operations.

“At BNY, we view AI as a transformative capability and have embraced its responsible use, having deployed almost 100 solutions that help streamline workflows across the company,” says Michael Demissie, Head of Applied AI and Practice, BNY. “AI is helping us serve clients more effectively, and is creating capacity for our employees to focus on higher-value activities.”

Efforts from these banks show that while operational and cybersecurity investments have more direct internal impact, they can also lead to more commercial success with small businesses.

“We’ve improved our speed to market a lot over the years by really focusing on implementing [technology], adding automations and really consolidating any technologies we’re using so we can be more efficient. There's an implementation cost to it, and you're not going to get the financial reward back as quickly. But what you are going to get is a customer where you wouldn't have gotten a customer."

- Community banker in Iowa

Demand for Current and Future Services

Our survey uncovered differing levels of alignment between community banks and small businesses on current and future services. The two groups are most aligned on current unmet demand for digital payments support, merchant services and faster loan approval. Notably, community banks we surveyed were overestimating the current demand from small businesses for industry-specific banking solutions, such as healthcare equipment financing, and underestimating the demand for expanded customer service hours.

In relation to future services, community banks and small businesses are largely aligned on the need for key offerings like cybersecurity and fraud prevention tools, as well as digital banking tools. Our study found there is one area where community banks are most underestimating a growing need amongst their small business clientele: business credit cards.

When we asked small business executives about what services they desire specifically from community banks, they selected business credit cards as the top choice at 35%. Yet when we asked community bankers what services they most want to deliver to their customers, only 23% selected credit card business. This presents a potential opportunity for community banks to capture demand from small businesses.

This high interest in credit card funding was also highlighted in the most recent Intuit QuickBooks Small Business Index, which found that rising interest rates have increased a reliance on credit cards as a primary source of funding for small business executives.6 The study also found that traditional, long-term loans for financing are increasingly being replaced with credit card funding.

“We’ve encountered an increase in credit card inquiries more than we have in the past. As rates go down, that demand will increase as businesses will have to pay less on interest. This positions us to explore offering credit cards to fill this financing gap, with the added incentive of attracting new clients and retaining current ones that are leveraging credit elsewhere."

- Reggie Webber, Chief Credit Officer, Optus Bank

CHAPTER 3: A LOOK AHEAD

In this year’s study, community bankers selected data analytics and insights capabilities as the biggest opportunity in the next five years, followed by expanding the digital banking services they offer. Focusing on these capabilities can enable the 1 in 5 community bankers who also deem targeted market segmentation and geographic expansion as major opportunities to grow relationships with current customers and capture new relationships in untapped markets.

“We have lots of data that could be better used to deliver value to customers. As we expand into new markets and customer segments, we’re making a deliberate effort to bring together information from all our business lines so that we can make genuine data-driven decisions as we expand. This will allow us to capture more opportunities, gain wallet share and deliver real value to our customers."

- Vance Smiley, Chief Operating Officer, Southern Bancorp

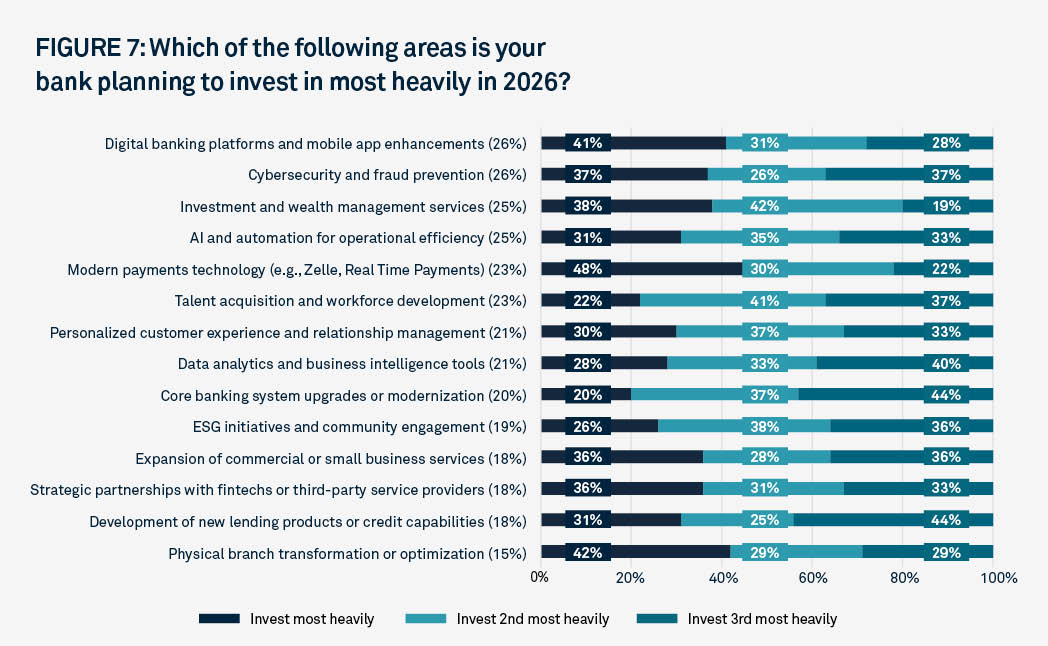

In the near term, our survey also shows that 2026 will see significant investments from community banks in AI, cybersecurity and fraud prevention, digital banking capabilities and modern payments technology. Over 1 in 5 (23%) of the community banks that participated in our survey ranked modern payments as a top investment priority, with 48% of these banks specifically noting capabilities like Real Time Payments as a primary focus area for next year.

As the economic landscape evolves rapidly and competition intensifies, community banks are hyper-focused on providing top-notch client service and modern technology solutions to their customers, which in turn will help ensure the stability of local markets and the entire U.S. economy.

“Community banks are more than financial institutions — they are the heartbeat of local economies, the stewards of trust and the architects of inclusive growth,” says Shofiur Razzaque, Head of Community Banking & Solutions, BNY. “As the financial landscape evolves, BNY is committed to supporting these institutions with the tools and insights they need to build a more resilient future.”